Aero Titans Boeing and Airbus: Who Will Seize the Day?

The venerable 105-year-old Boeing Company has been locked in competition with 21-year-old Airbus SE, which was born from the culmination of various historic European aircraft manufacturers who consolidated after the Second World War and with about 25% of its stock held by the governments of France, Germany and Spain. The latter surpassed the former as the world’s largest plane maker by the end of 2019 and is intent on maintaining its lead.

In order to analyze the value propositions of the companies, which is inherent to determine their investment potential, the scenario can be broken down simply based on market type: civilian versus military.

Civilian Market

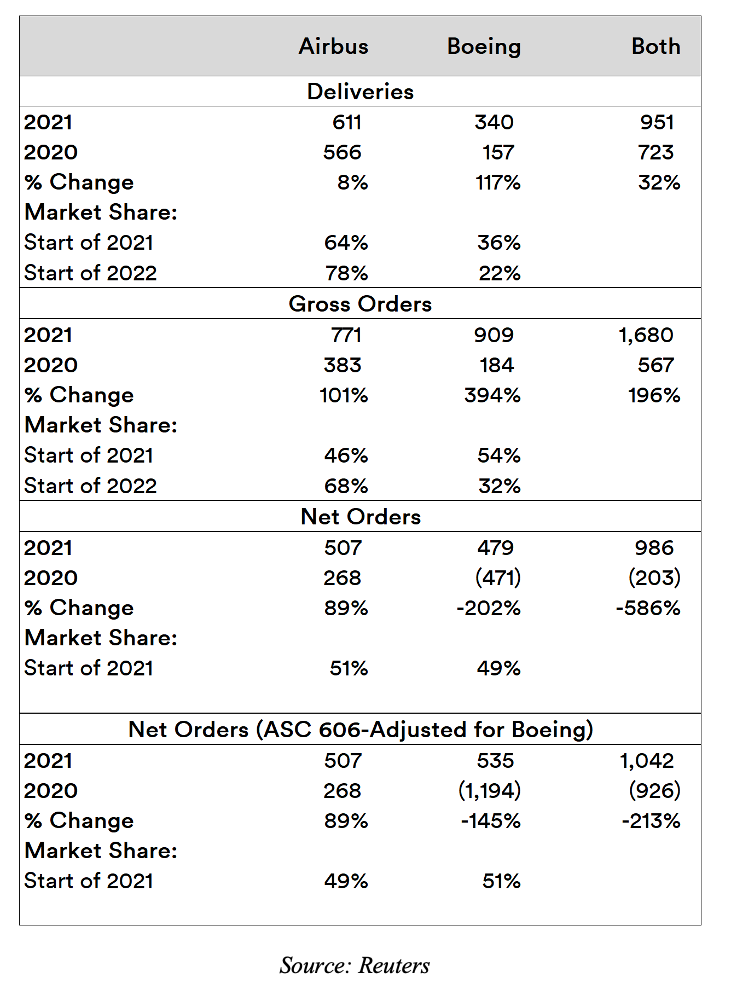

For the year 2021, Reuters had reported that while Airbus had delivered more aircrafts than Boeing, the latter had recovered by the end of the year in terms of gross orders.

In terms of net orders (gross orders minus cancellations or conversions), Boeing remains a little behind. This metric improves after Boeing adjusts the net orders as per ASC 606 (an accounting mechanism that filters out past orders of aircrafts deemed unlikely to be delivered, due to the financial condition of the buyers).

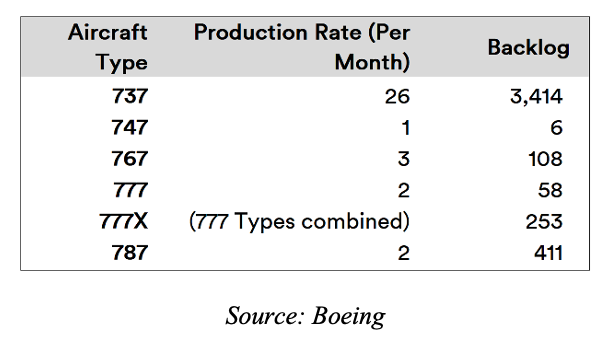

Boeing has the highest production capability in the problematic model 737 – which is also its largest backlog as of end of 2021.

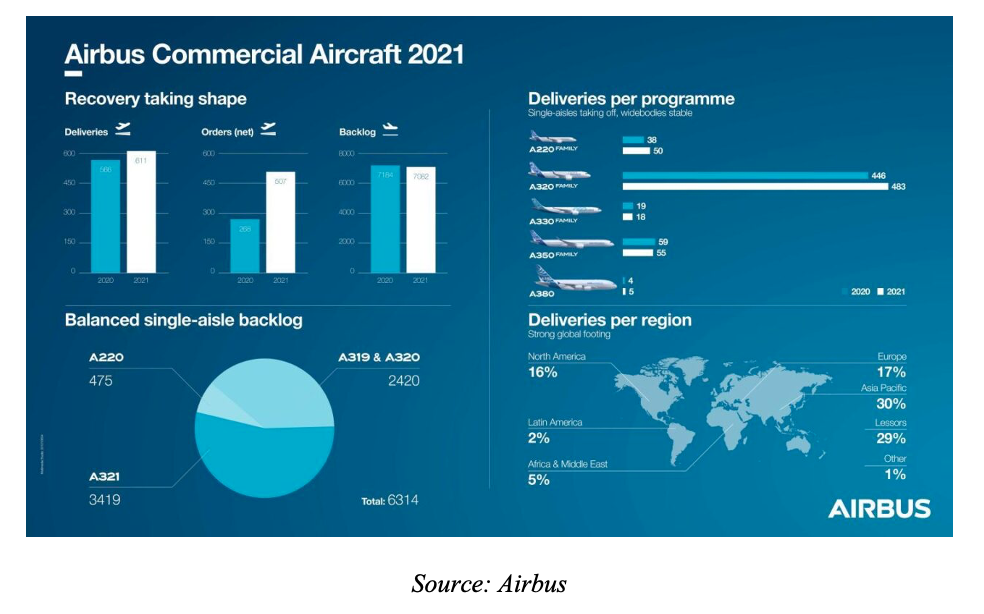

Meanwhile, as of end of February this year, Airbus’ reports on its net total in terms of orders and deliveries indicate prevailing strength.

2021 witnessed a massive increase in Airbus’ orders, a slight increase in deliveries and a slight decrease in backlog when compared to 2020. This indicates that the European manufacturer has gone from strength to strength during the pandemic.

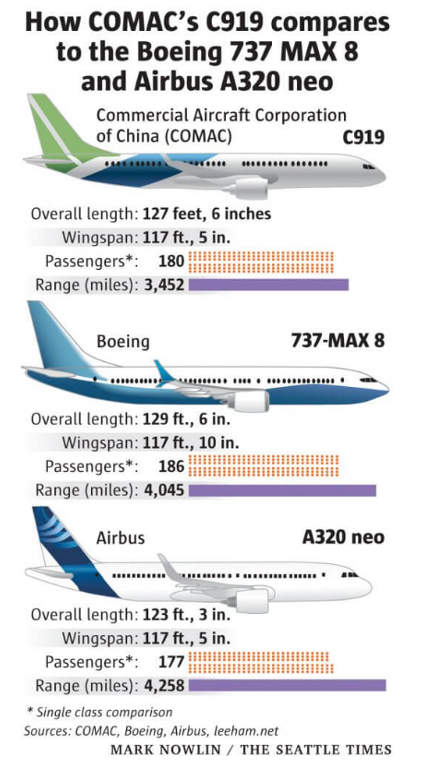

However, both titans have new rivals that are steadily building competing product offerings. Over the past couple of years, the Commercial Aircraft Corporation of China (COMAC) – a corporation owned predominantly by the Chinese government – has been working on the C919 which, as of late 2021, has reported to be ready to commence deliveries later in 2022, with China Eastern Airlines being its launch customer.

Like most commercial aircraft manufacturers, COMAC is heavily dependent on Western suppliers. In fact, it has been reported that up to 60% of its parts come from the likes of Honeywell and General Electric.

Another rising competitor is the PJSC United Aircraft Corporation (or “Obyedinyonnaya Aviastroitelnaya Korporatsiya” in its native Russian, with a Moscow Stock Exchange ticker “UNAC”) which is predominantly a conglomerate comprising of the Soviet-era Ilyushin, Irkut, Mikoyan, Sukhoi, Tupolev and Yakovlev design bureaus, with a majority stake held by the Russian government. UNAC’s Irkut MC-21 (which is largely similar to the C919 except in the engines) is also expected to take flight this year.

Like the C919, the MC-21 is also dependent on Western suppliers such as Raytheon’s Collins Aerospace and Honeywell. As Russia’s “special military action” in Ukraine continues, most of these suppliers have complied with sanctions and are pulling out of assisting in development of UNAC’s civilian aircraft initiative. This is expected to create significant delays, of at least a few years, for a large-scale rollout of the MC-21. In June 2016, both UNAC and COMAC initiated a joint venture company named the “China-Russia Aircraft International Co, Ltd.” (CRAIC), in Shanghai, with the intention of producing long-range 250- to 320-seat widebody airliners by 2028. Given the problems faced by Russian companies, it is likely that this timeline will suffer as well.

Military Market

The military market is very complicated. After the Cold War ended and the Soviet Union dissolution, the military aircraft market is now open to competition from all quarters, as opposed to being limited within geopolitical silos. Russian arms manufacturers have found markets in over 45 countries as of 2020.

Its largest military market by far was the Republic of India which has the world’s second largest military and is the third largest military spender. At the time of the Soviet Union’s breakup, over 70% of the India’s army armaments, 80% of its aviation systems and 85% of its naval platforms were of Soviet origin. However, over this past decade, the share of Russian arms imports in India fell from 70% in 2012-17 to 46% in 2017-21.

This has primarily been of benefit to manufacturers in France, Israel and the United States. Boeing benefited enormously too. Of the various military products made by the company, the Indian military operates the world’s second largest fleet of P8I submarine hunters after the United States., 22 Apache helicopter gunships built with India-specific requirements, 15 Chinook transport helicopters, as well as 11 C-17 Globemaster III heavy transport aircrafts. However, the outlook for future orders looks cloudy on account of an increasing push on foreign manufacturers to either set up bases in India by themselves, to produce a substantial proportion of the systems being purchased, or to initiate joint ventures with Indian companies who have Indian employees and facilities.

Most of Boeing’s purchases were made under the previous military imports regulations, which required an “offset”, meaning that for every weapon system being introduced via a foreign manufacturer, said manufacturer must set up a certain number of localized production-related facilities in India and must select a certain number of system or sub-system suppliers from among India’s high-tech enterprises. However, a key component of the United States government policy is the leveraging of arms exports to maintain its industrial base and — through economies of scale — to reduce costs to the U.S. armed forces. Thus, Boeing has been unable to comply with offsets under the previous law, and is facing difficulties in maintaining sizeable production work under the current law, in order to sell military products in India.

In contrast, Airbus has registered significant success recently. In a deal made in September 2021, the company secured the sale of 56 C-295 tactical transporters to the Indian military. After an outright import of 16 aircrafts in fully-prepared condition, the company will be developing an entire industrial ecosystem – from manufacturing, assembly, testing and qualification, to delivery and maintenance over the aircraft’s lifecycle – in a joint venture with its partner Tata Advanced Systems Limited (TASL). The company undoubtedly hopes to leverage this new industrial base to drive future sales of other aircrafts and thus deepen market penetration.

In previous years, after a deal for 126 Rafale fighter jets by French company Dassault Aviation was watered down to 36 in “fly-away” condition by the Indian government, the French government – also a key stakeholder in Airbus – pitched a proposal to set up a completely indigenous production facility for manufacturing Rafales if the deal size was pushed up to 100. Additionally, French engine manufacturer Safran offered to modernize and co-develop the indigenous Kaveri engine. After 30 years of intensive work which resulted in nine full prototype engines, four core engines and strong capabilities developed in many critical technology domains, this engine was passed over to meet the changing requirements of the Indian Light Combat Aircraft program – which opted for General Electric engines instead. The French government guaranteed that Safran’s proposal will ensure the republic’s complete ‘sovereignty’ in aero-engine technology. Given how seriously both the Indian government and its billion-plus citizens take the notion of sovereignty, this is a very canny offer and, unsurprisingly, is in the final stages of discussion.

These sorts of innovative decision-making by European players (as well as Israeli companies) indicate why the likes of Boeing and UNAC are finding it so challenging to make inroads in this massive market. The latter, particularly, has floundered in effectively meeting the Indian government’s stringent requirements in areas such as quality, efficiency and timely delivery when it comes to new orders of next-generation aircraft (as opposed to upgrades and spares for Soviet-era acquisitions). Also, an order placed with Boeing to acquire six additional P8I aircraft in 2019 was cancelled earlier this year in favor of an indigenous platform based on locally-produced Airbus C-295.

Given the complexity of this market, it is difficult to take a call on which company will perform best in weapons sales all over the world. In India’s case, however, Airbus is increasingly stronger in terms of positioning over both Boeing and UNAC.

Ratios and Trends

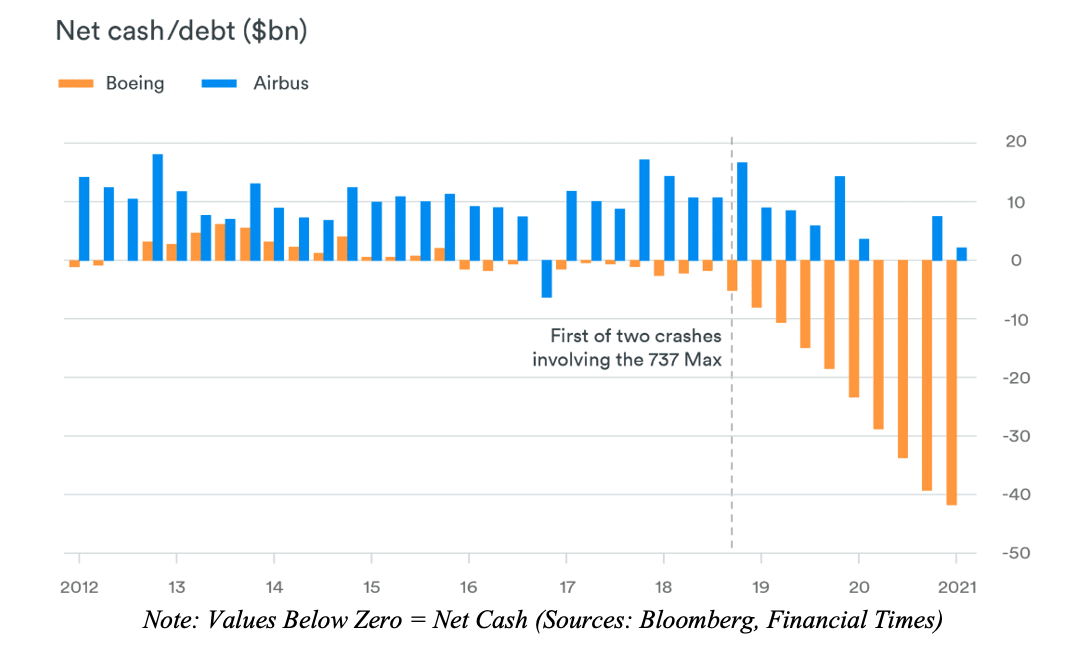

With regard to fiscals, Boeing showed very strong net cash positions relative to Airbus while going into 2021:

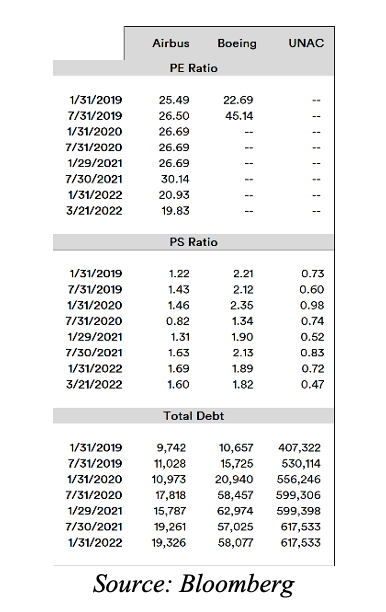

While this might suggest that Boeing was in a strong position, this was more attributable to the fact that the reduction in orders on account of problems with the 737 Max had lowered expenses. This supposition is validated by the Price-to-Earnings (PE) Ratios of Boeing, on par with UNAC. While Boeing’s Price-to-Sales (PS) Ratios led over Airbus for a while, both companies’ PS Ratios are now beginning to draw par. UNAC is a laggard in this metric.

Debt is not a huge concern given the sheer size of these companies. Nonetheless, in this metric, UNAC leads the pack, with Boeing being next (with predominantly long-term debt). Airbus has also recently been packing on long-term debt (which now constitutes around 89% of its total debt).

Note: Data services don’t report ratios if they’re deemed meaningless. When earnings go negative, PE Ratios estimates go negative. Given that stock price is always positive, this is considered “meaningless”.

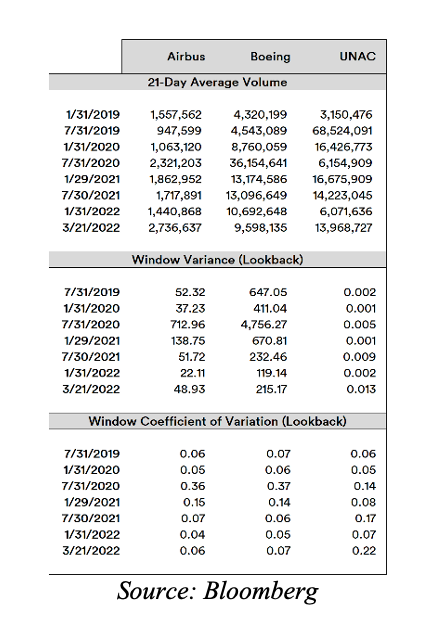

In the time horizons created between the dates shown above, the stock performance has been quite interesting. UNAC’s stock price had been and remains absurdly low – thus aiding in creating solid average daily traded volumes (in units of shares). In comparison, Airbus has been the least traded. Boeing’s stock performance on the other hand, has shown extremely high variance. This price trajectory is unsurprising- after all, the U.S. equity market is the most overvalued in the world and overvaluation leads to volatility. Airbus comes second here, with UNAC running relatively flat across all the windows.

There is very strong similarity in the extent of variability of stock prices between Boeing and Airbus within each horizon, as demonstrated by the coefficient of variation. UNAC had a fairly similar trend as well, until Russia’s recent actions in Ukraine pushed up both this metric and daily volumes.

In Conclusion

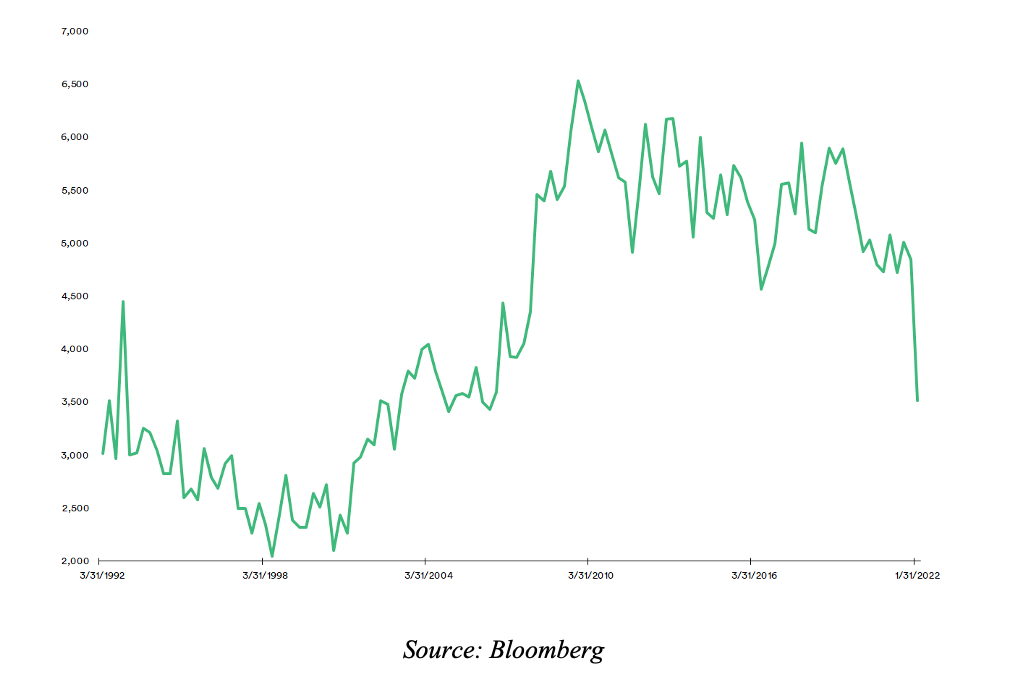

The mercurial nature of the global military market means that Boeing will likely have to predominantly rely on its domestic legacy business in the U.S. The trend seen in U.S. military aircraft shipments, which started rising after 2001 after a decade of decline, has been downwards since 2010.

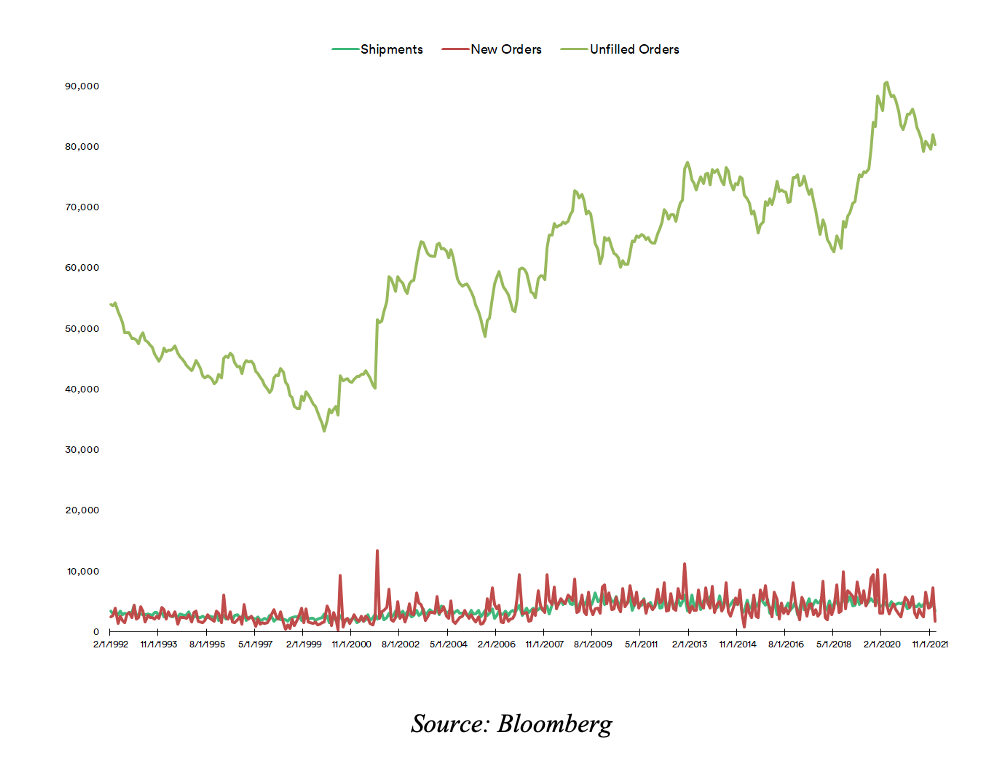

While new orders and shipments have been keeping pace with each other over the past several years, the net value of unfilled orders in the U.S. market continue to balloon upwards.

The sheer size of “Unfilled Orders” needs some context: while new systems are constantly proposed and even approved, the long timelines for system development vis-à-vis changes in strategic needs and changing technologies means that a large proportion of these orders (by value) will be in limbo until they’re replaced by other orders – after which the cycle repeats. This is, by no means, unique to the United States, as other nations’ spending shows similar trends. However, none are quite as massive as in the United States. This is an additional factor that highlights the complexity of the military market.

Like UNAC, Boeing has a massive legacy business because of its longevity. Unlike UNAC, it has an element of diversification, by virtue of the vast fleets of commercial aircrafts already sold internationally, which will inevitably lead to at least some repeated business. The latest development – a China Eastern Airlines Boeing 737-800 taking a near-vertical fall into the Guangxi Hills in southern China – will potentially raise many questions of the company’s technical competency, which will possibly get murkier in the upcoming months of investigation and will likely have some impact on the company’s stock performance in the near term.

In the current day, Boeing and Airbus are effectively a duopoly in the civilian market, which is quite meaningful in terms of business. Over the mid- to long-term (i.e. around 5-10 years), an investor shouldn’t be surprised if new rivals emerge: be it COMAC, UNAC or even an Indian company or conglomerate that suddenly announces an entry into this space. Until then, while both companies are viable mid- to long-term investments, Airbus is slightly better positioned than Boeing in terms of nimbleness, market prospects, and perceived technical competence. What this picture will look like in a year’s time is, of course, another matter.

For investors in the near term, based on current events, a number of strategies can be considered with leveraged, inverse or “leveraged inverse” gains by investing in the 3X Long Boeing ETP (ISIN: XS2297551371), 3X Long Airbus ETP (ISIN: XS2399366280), -1X Short Boeing ETP (ISIN: XS2297551454) or the -3X Short Airbus ETP (ISIN: XS2399367171) or combinations of thereof.

It also bears remembering that with movement restrictions due to the pandemic, a related sector – airlines – had been picking up momentum and volumes. The ongoing airspace restriction over Russia has led to a simultaneous increase in travel costs as well as a negative outlook which might not last for very long, as travel normalizes around this recent situation. For tactical short-term investment strategies in this sector, investors can consider the 3X Long Airlines ETP (ISIN: XS2399369383) or the -3X Short Airlines ETP (ISIN: XS2399369466). Both of these products are based on the U.S. Global Jets ETF which is comprised of 50 airline operators, air cargo operators, travel booking companies and aircraft manufacturers from all over the world – including both Boeing and Airbus.

Podcast

Podcast